加载中…

加载中…America and China, the Next Major War

标签:

财经 |

分类: 大势 |

By: Clif_Droke

In the current phase of relative peace and stability we now

enjoy, many are questioning when the next major war may occur and

speculation is rampant as to major participants involved. Our

concern here is strictly of a financial nature, however, and a

discussion of the geopolitical and military variables involved in

the escalation of war is beyond the scope of this commentary. But

what we can divine from financial history is that “hot” wars in a

military sense often emerge from trade wars. As we shall see, the

elements for what could prove to be a trade war of epic proportions

are already in place and the key figures are easily

identifiable.

Last Wednesday the lead headline in the Wall Street Journal

stated, “Business Sours on China.” It seems, according to WSJ, that

Beijing is “reassessing China’s long-standing emphasis on opening

its economy to foreign business….and tilting toward promoting

dominant state companies.” Then there is Internet search giant

Google’s threat to pull out of China over concerns of censorship of

its Internet search results in that country.

The trouble started a few weeks ago Google announced that it no

longer supports China’s censoring of searches that take place on

the Google platform. China has defended its extensive censorship

after Google threatened to withdraw from the country.

Additionally, the Obama Administration announced that it backs

Google’s decision to protest China’s censorship efforts. In a

Reuters report, Obama responded to a question as to whether the

issue would cloud U.S.-China relations by saying that the human

rights would not be “carved out” for certain countries. This marks

at least the second time this year that the White House has taken a

stand against China (the first conflict occurring over tire

imports).

Adding yet further fuel to the controversy, the U.S. Treasury

Department is expected to issue a report in April that may formally

label China as a “currency manipulator,” according to the latest

issue of Barron’s. This would do nothing to ease tensions between

the two nations and would probably lead one step closer to a trade

war between China and the U.S.

Then there was last week’s Wall Street Journal report concerning

authorities in a wealthy province near Shanghai criticizing the

quality of luxury clothing brands from the West, including Hermes,

Tommy Hilfiger and Versace. This represents quite a change from

years past when the long-standing complaint from the U.S. over the

inferior quality of Chinese made merchandise.

On Monday the WSJ ran an article under the headline, “American

Firms Feel Shut Out In China.” The paper observed that so far

there’s little evidence that American companies are pulling out of

China but adds a growing number of multinational firms are

“starting to rethink their strategy.” According to a poll conducted

by the American Chamber of Commerce in China, 38% of U.S. companies

reported feeling unwelcome in China compared to 26% in 2009 and 23%

in 2008.

As if to add insult to injury, the high profile trial of four Rio

Tinto executives in China is another example of the tables being

turned on the West. The executives are by Chinese authorities of

stealing trade secrets and taking bribes. There’s a touch of irony

to this charge considering that much of China’s technology was

stolen from Western manufacturing firms which set up shop in that

country.

It seems China is flexing its economic and political muscle against

the West in a show of bravado. Yet one can’t help thinking that

this is exactly the sort of arrogance that typically precedes a

major downfall. As the Bible states, “Pride goeth before

destruction, and an haughty spirit before a fall.”

In his book, “Jubilee on Wall Street,” author David Knox Barker

devotes a chapter to how trade wars tend to be common occurrences

in the long wave economic cycle of developed nations. Barker

explains his belief that the industrial nations of Brazil, Russia,

India and China will play a major role in pulling the world of the

long wave deflationary decline as their domestic economies begin to

develop and grow. “The are and will demand more foreign goods

produced in the United States and other markets,” he writes. Barker

believes this will help the U.S. rebalance from an over weighted

consumption-oriented economy to a high-end producer economy.

Barker adds a caveat, however: if protectionist policies are

allowed to gain force in Washington, trade wars will almost

certainly erupt and. If this happens, says Barker, “all bets are

off.” He adds, “The impact on global trade of increased

protectionism and trade wars would be catastrophic, and what could

prove to be a mild long wave [economic] winter season this time

around could plunge into a global depression.”

Barker also observes that the storm clouds of trade wars are

already forming on the horizon as we have moved further into the

long wave economic “winter season.” Writes Barker, “If trade wars

are allowed to get under way in these final years of a long wave

winter, this decline will be far deeper and darker than necessary,

just as the Great Depression was far deeper and lengthier than it

should have been, due to growing international trade

isolationism.

He further cautions that protectionism in Washington will certainly

bring retaliation from the nations that bear the brunt of punitive

U.S. trade policies. He observes that the reaction from one nation

against the protectionist policies of another is typically far

worse than the original action. He cites as an example the

restriction by the U.S. of $55 million worth of cotton blouses from

China in the 1980s. China retaliated by cancelling $500 million

worth of orders for American rain. “As one nation blocks trade, the

nation that is hurt will surely retaliate and the entire world will

suffer,” writes Barker.

Barker comments that a major trade conflict between the United

States and some of its trading partners may be inevitable due to

the protectionist tendency of the current Congress. “When the world

plunges deeper into the long wave decline and barriers are thrown

up everywhere to protect ailing industries that have expanded

beyond world demand for their goods with expensive debt,” writes

Barker, “the situation could force major changes.”

Sounding an optimistic note he concludes, “Let us hope that

leadership emerges that can take a trade crisis during this long

wave winter to produce sweeping positive changes in the form of new

free trade agreements for the global trading system. It is possible

that we maintain free and open markets and go in the direction of

greater free trade for the next long wave advance, since we are

only a few years away.”

There seems to be an emerging consensus among investors that China

is “decoupling” from the West and has developing its own domestic

markets to the point where it needs no longer to rely on export

growth to the U.S. for its economy strength. As debatable as this

prospect is (and there are valid arguments on both sides), our main

focus is on the financial outlook for China. Two things stand out.

The first is that the iShares China 25 Index Fund (FXI), our proxy

for the China stock market, has been notably lagging the recovery

in the U.S. broad market S&P 500 index in the past

few months. While the U.S. stock market has recently made an

18-month high, shares of Chinese companies as measured by FXI are

still below their previous high from November 2009.

What’s interesting to note is that not only has there been a

decoupling from the U.S. stock market, but the China stock market

has been closely correlated to movements in the price of gold,

especially in the last several months. Comparing the FXI to the

SPDR Gold Trust ETF (GLD), a proxy for the gold price, the similar

trajectories can be easily seen. China’s appetite for gold is well

known and until its near term financial condition improves it’s

likely that the gold price will move more or less in harmony with

China’s stock market, as has been the case in recent months.

http://www.marketoracle.co.uk/images/2010/Mar/fxi-27.gifand

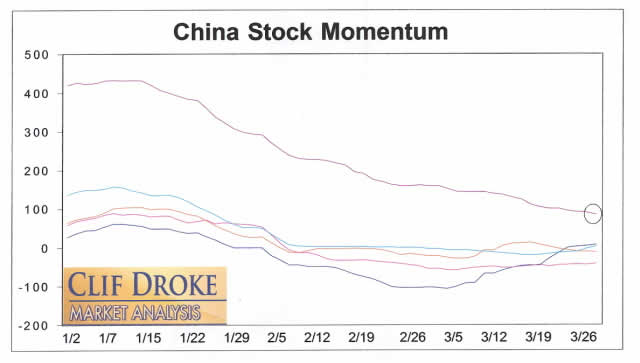

Another observation is that the China stock internal momentum

indicator series (CHINAMO) is showing far less internal strength

than the broad market NYSE index shown above. Moreover, the

dominant longer-term indicator for the China stocks (circled) has

been in a sustained decline for the past few months. This is

reminiscent of what the long-term NYSE hi-lo momentum index looked

like in 2007 heading into the credit crisis. Beyond a short-term

rally, which is possible based on the near term internal rate of

change for China shares, the longer-term momentum structure for

Chinese stocks is troubling. Unless it shows substantial

improvement in the weeks and months ahead, it could set the stage

for further trade disputes. As we observed in last week’s

commentary, prolonged trading ranges always elicit the worst sort

of emotions among investors. Governments are no more immune to the

negative psychological effects of financial market stagnation than

individual investors.

http://www.marketoracle.co.uk/images/2010/Mar/chinamo-27.jpgand

It’s evident that as much as China’s internal markets are

developing, that nation is still heavily reliant on the U.S.,

whether it wants to formally admit it or not. For this reason, a

trade war between the two nations would prove catastrophic and one

can see how a trade war between these two economic titans could

easily escalate into something far more destructive. Touching on

this issue in his latest book, “The Ascent of Money,” author Niall

Ferguson asks, “Could anything trigger another breakdown of

globalization like the one that happened in 1914 [leading to World

War I]? The obvious answer is a deterioration of political

relations between the United States and China, whether over trade,

Taiwan, Tibet or some other as yet subliminal issue.”

He further comments, “Scholars of international relations would no

doubt identify the systemic origins of the war in the breakdown of

free trade, the competition for natural resources or the clash of

civilizations….Some may even be tempted to say that the surge of

commodity prices in the period from 2003 until 2008 reflected some

unconscious market anticipation of the coming conflict.”

This brings us to the crux of the matter, namely, when can we

expect to see the chimera of war rear its ugly head (or heads) once

again? In my recent book on the Kress Cycles, “The Stock Market

Cycles,” I identified the Kress 24-year cycle as the War Cycle

since it’s bottoming has always coincided with a major outbreak of

war. The latest 24-year cycle is scheduled to bottom in 2014 along

with the Master Cycle of 120 years. The final “hard down” phase of

any cycle is always the last 8-12% of the cycle’s length. This

means that we can most likely expect to see an eruption of major

war sometime in the latter part of 2011 to the year 2012, up until

the cycle bottom in 2014. The last of the major yearly cycles,

namely the 6-year cycle, will peak in later 2011. This should

afford the global economy with more time to rest and recuperate

from the effects of the late credit crisis and build up their war

chests before the next “big one” begins. Now is the time to fear a

sudden outbreak of war, which is unlikely just yet. Instead, it’s a

time for the small investor to take advantage of the final “peace

phase” by focusing on opportunities in the financial markets as

they continue to emerge in this recovery.

{kind=link}

{kind=link}

![]() 喜欢

喜欢

0

![]() 赠金笔

赠金笔